Press releases

First-Half 2018 Results

Corporate & other activities, Finance

Paris, 26 July 2018

Lagardère revises upwards its Group recurring EBIT(1) target for 2018: growth now expected between 1% and 3%(2)

Sustained revenue growth, up 4.4% like-for-like(1)

- Revenue of €3,366 million, up 4.4% like-for-like(1)

- Group recurring EBIT(2) stable, lifted by strong business momentum despite an unfavourable sporting calendar

- Profit before finance costs and tax up sharply to €243 million from €95 million in first-half 2017(3)

- Solid financial position with free cash flow improving substantially to a positive €149 million from a negative €67 million in first-half 2017(3)

The Group is actively pressing ahead with its strategic refocusing plan, with the closing this half of several significant transactions, including the completion of the sale of the Radio assets in the Czech Republic, Poland, Slovakia and Romania, the agreement reached for the sale of magazine titles in France, the sale of the e-Health unit and the disposal of the stake in Marie Claire.

The Lagardère group maintained solid growth momentum in the first half, despite a subdued calendar, illustrated by the good performance of Lagardère Travel Retail, and sustained business levels across the other divisions.

- Robust Group business

- The Group’s revenue came in at €3,366 million in first-half 2018, up 4.4% like-for-like. The increase mainly reflects strong growth at Lagardère Travel Retail (up 9.9% like-for-like), as well as a solid contribution from Lagardère Publishing and Lagardère Active despite the unfavourable market environments.

- Group recurring EBIT stable

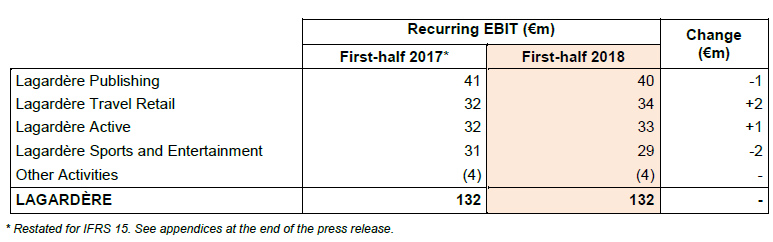

- Group recurring EBIT remained stable year on year(3), at €132 million, driven by solid growth at Lagardère Travel Retail, as well as by a good performance from Lagardère Sports and Entertainment despite an unfavourable sporting calendar effect.

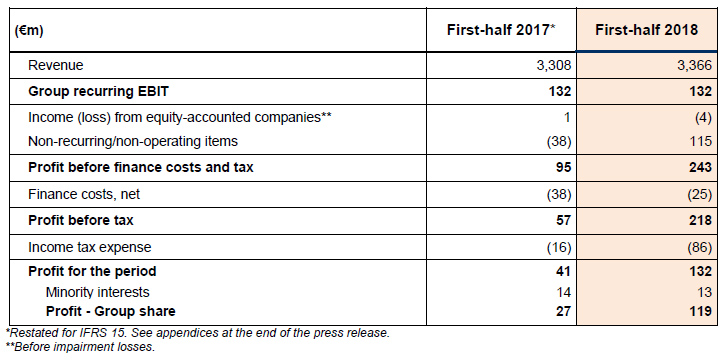

- Profit before finance costs and tax advanced sharply to €243 million from €95 million in first-half 2017(3).

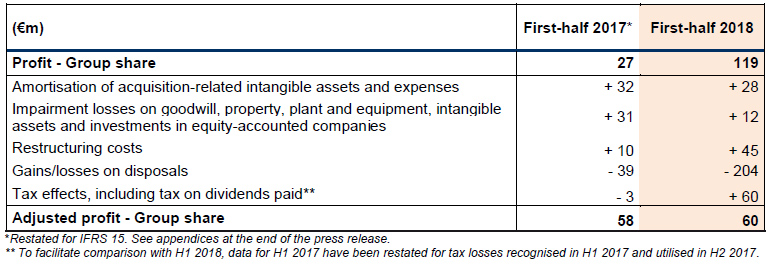

- Profit – Group share came out at €119 million versus €27 million in the prior-year period. Adjusted net profit – Group share rose to €60 million from €58 million in the six months to 30 June 2017(3).

- Solid financial position

- Free cash flow improved substantially to a positive €149 million from a negative €67 million in first-half 2017, owing essentially to the improvement in working capital.

- The leverage ratio (net debt(1)/recurring EBITDA(1)) improved year on year to 2.3x versus 2.6x in first-half 2017(3), reflecting the Group’s tight rein on debt as well as the positive impact of cash generation in the first half of 2018.

I- REVENUE AND RECURRING EBIT

REVENUE

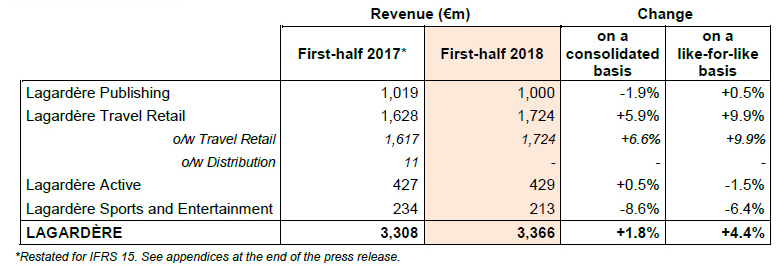

In the first half of 2018, Lagardère group revenue totalled €3,366 million, up 4.4% like-for-like (up 1.8% on a consolidated basis).

The difference between consolidated and like-for-like revenue is mainly attributable to a €110 million negative foreign exchange effect resulting chiefly from the depreciation of the US dollar. Changes in scope of consolidation had a positive €25 million impact, essentially relating to acquisitions carried out by Lagardère Publishing and Lagardère Travel Retail, partially offset by the divestment of Press Distribution operations in Hungary.

First-half 2018 revenue:

RECURRING EBIT

Lagardère Publishing

Revenue

Revenue totalled €1,000 million, up 0.5% like-for-like (down 1.9% on a consolidated basis). The difference between consolidated and like-for-like revenue is attributable to a €42 million negative foreign exchange effect resulting mainly from the depreciation of the US dollar, and an €18 million positive scope effect, due notably to the 2017 acquisitions of Bookouture, Jessica Kingsley, Summersdale and IsCool Entertainment.

Business was up slightly in the first half of 2018, buoyed chiefly by growth in General Literature in France and a good performance in Partworks. These positive factors helped overcome the unfavourable comparison basis resulting from Spain’s curricular reform campaign in 2017.

The figures below are presented on a like-for-like basis.

In France growth of 2.5% was chiefly driven by General Literature, boosted by the success of Guillaume Musso’s La Jeune fille et la nuit, and by very good momentum at Le Livre de Poche paperbacks. Distribution was also on an upward trend, buoyed by a number of best-selling titles.

Business levels eased back in the United Kingdom (down 2.5%), where the success of Michael Wolff’s Fire and Fury at Little, Brown Book Group did not offset the full effect of the contraction in the frontlist at Headline and Hodder.

The 1.4% uptick in revenue in the United States mainly reflected the success of the James Patterson and Bill Clinton novel The President is Missing together with a sustained release schedule at Perseus, which offset the contraction at Nashville following the success of Paul Young’s The Shack in first-half 2017.

The Spain/Latin America region was down 5.1%, owing to an unfavourable comparison effect, with the first-half 2017 performance having benefited from the earlier and higher-volume textbook campaign in Spain. Excluding these effects, however, business held firm.

Partworks maintained its positive trend (up 2.7%), driven by the continued success of core collections in Latin America especially, and by a busy programme of new title launches in France and Italy.

E-books accounted for 8.4% of Lagardère Publishing revenue in first-half 2018, compared to 8.8% in first-half 2017.

Recurring EBIT

Recurring EBIT amounted to €40 million in first-half 2018, down €1 million. Positive momentum in General Literature in France and improved profitability in the United States only partly offset the downturn in business in Spain (held back by the tough comparison basis due to the earlier and higher-volume textbook campaign in first-half 2017), and the slight decline in the United Kingdom.

Lagardère Travel Retail

Revenue

Revenue totalled €1,724 million, up 9.9% like-for-like (up 5.9% on a consolidated basis). The difference between like-for-like and consolidated revenue reflects a €60 million negative foreign exchange effect due mainly to the depreciation of the US dollar, and a negative €4 million scope effect, chiefly attributable to the divestment of Press Distribution operations in Hungary but partially offset by the consolidation of IFS Duty Free stores in Poland.

The figures below are presented on a like-for-like basis.

Travel Retail delivered robust 9.9% growth in first-half 2018, lifted by strong sales momentum, network expansion and store openings in the EMEA and Asia-Pacific regions.

In France, revenue continued to advance slightly, up 1.4%, buoyed mainly by a positive network effect in Foodservice which more than offset the adverse impact of transport strikes.

The EMEA region (excluding France) made strong gains (up 13.4%), mainly reflecting sparkling sales performances in Eastern Europe as well as network expansion in Switzerland (Geneva), Poland (Gdansk) and Senegal (Dakar).

North America reported good momentum (up 2.7%), lifted by growth in Foodservice and by robust passenger traffic despite an adverse short-term network impact.

The Asia-Pacific region posted stellar revenue growth (up 32.1%), with Asia continuing to benefit from the launch of the new Hong Kong concession and from expansion in Fashion and Foodservice in China. Revenue in the Pacific region was lifted by a good performance in Australia and by the impact of Duty Free store refurbishments in Auckland, New Zealand.

Recurring EBIT

Recurring EBIT amounted to €34 million in first-half 2018, up €2 million, on the back of organic growth in the EMEA region, especially Italy and Poland, and in North America, as well as by one-off cost reductions which offset the adverse impact of transport strikes in France and start-up costs of new operations.

Lagardère Active

Revenue

Revenue totalled €429 million, down 1.5% like-for-like (up 0.5% on a consolidated basis). The difference between like-for-like and consolidated figures is attributable to an €8 million positive scope effect primarily resulting from the acquisitions of Aito Media Group in October 2017 and of Skyhigh TV in March 2018.

The figures below are presented on a like-for-like basis.

Revenue in the first half of 2018 held firm, thanks to good performances posted by International Radio and TV activities, as well as positive trends for Pure Digital and B2B, which together offset the limited contraction in Press revenue and the impact of lower audience figures for the Europe 1 radio station over the period.

Magazine Publishing revenue was resilient, with the contraction contained at 3.3% amid a downturn in the advertising and circulation markets. Advertising revenues fell 6.7% year on year, while circulation remained more or less flat (down 1.2%).

Revenue for the Radio segment retreated 3.3%, with a strong performance from International Radio somewhat offsetting lower audience figures for the Europe 1 radio station over the period.

TV activities remained on a positive track (up 1.5%), lifted by higher TV channel advertising revenues and by well-executed programme deliveries on the international segment by Lagardère Studios.

Pure Digital and B2B revenue gained 3.1%, buoyed mainly by positive momentum in e-Health (MonDocteur).

Advertising revenues for Lagardère Active as a whole (excluding International Radio) fell 6.1% over the period.

Recurring EBIT

Recurring EBIT amounted to €33 million in first-half 2018, up €1 million. The increase reflects the effects of the ongoing cost reduction plans in the Press segment together with the solid contribution from International Radio, which helped offset a lacklustre performance at the Europe 1 radio station and the adverse mix effect at Lagardère Studios.

Lagardère Sports and Entertainment

Revenue

Revenue totalled €213 million, down 6.4% like-for-like (down 8.6% on a consolidated basis). The difference between consolidated and like-for-like revenue can be explained by an €8 million negative foreign exchange effect linked primarily to the depreciation of the US dollar and a €3 million positive scope impact associated with the acquisition of Brave Marketing Ltd in 2017.

As expected, the fall in revenue is mainly attributable to an unfavourable sporting calendar in the football business as the Total Africa Cup of Nations and the Asian qualifiers for the 2018 FIFA World Cup were held in first-half 2017. Moreover, the successful Phil Collins tour in France in 2017, means that first-half 2018 revenues in Lagardère Live Entertainment are also down in comparison. This decline is partially offset by the successful delivery of the Gold Coast 2018 Commonwealth Games, the strong performance of sponsorship activities in Europe as well as the opening of the Bordeaux Métropole Arena and Arena du Pays d’Aix.

Recurring EBIT

Recurring EBIT amounted to €29 million, down slightly by €2 million, reflecting the adverse impact of an unfavourable calendar mainly in Africa and Asia, partially offset by the successful delivery of the Gold Coast 2018 Commonwealth Games as well as the good performance delivered by sponsorship activities in Europe.

Other Activities

Recurring EBIT from Other Activities remained stable year on year at a negative €4 million, with the beneficial effects of the ongoing overhead cost reduction plan offsetting the tough comparison basis in 2017 which included proceeds from the recovery of VAT.

II- MAIN INCOME STATEMENT ITEMS

NON-RECURRING/NON-OPERATING ITEMS

Non-recurring/non-operating items represented net income of €115 million, and mainly comprised:

– €45 million in restructuring costs, including €37 million at Lagardère Active, mainly as a result of a provision set aside to cover its ongoing restructuring into standalone units as part of the Group’s strategic refocusing plan, and €6 million at Lagardère Publishing, relating mainly to the streamlining of distribution centres in the United Kingdom.

– €205 million in net gains on disposals, including a €245 million gain further to the sale in May 2018 of an office building in the eighth arrondissement of Paris (France) that previously hosted Lagardère Active’s Radio and TV channel teams, and a €40 million loss booked on the disposal of the Group’s 42% stake in the Marie Claire group.

– €13 million in impairment losses against property, plant and equipment and intangible assets, including €9 million attributable to Lagardère Active resulting from the writedown of a portion of the goodwill relating mainly to Pure Digital entities.

– €32 million in amortisation of intangible assets and costs relating to the acquisition of consolidated companies, including €26 million for Lagardère Travel Retail, €3 million for Lagardère Publishing, €2 million for Lagardère Active and €1 million for Lagardère Sports and Entertainment.

FINANCE COSTS, NET

Net finance costs amounted to €25 million for first-half 2018, an improvement of €13 million on the prior-year period, chiefly reflecting the reduction in the Group’s average interest rate between the two periods, further to the debt refinancing carried out in 2017.

INCOME TAX EXPENSE

Income tax expense for first-half 2018 came to €86 million, and includes notably the tax payable on the disposal by Lagardère Active of an office building in the eighth arrondissement of Paris (France) in an amount of €83 million. The increase in income tax expense versus the first half of 2017 (€16 million), can mainly be explained by the increase in the tax charge arising on property disposals.

PROFIT

Taking account of all these items, profit came out at €132 million, including €119 million attributable to the Group.

ADJUSTED PROFIT – GROUP SHARE

III- OTHER FINANCIAL INFORMATION

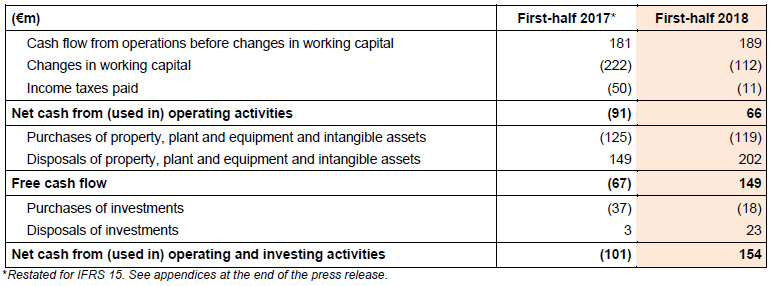

NET CASH FROM (USED IN) OPERATING AND INVESTING ACTIVITIES

- Net cash from operating activities

– Cash flow from operations before changes in working capital amounted to €189 million, up €8 million on the prior-year period. The higher figure in first-half 2018 reflects a decrease in disbursements for restructuring across all divisions.

– Changes in working capital (typically negative in the first half) improved substantially during the period, representing an outflow of €112 million in first-half 2018 compared to an outflow of €222 million in the six months to 30 June 2017. This improvement is attributable to the working capital optimisation drive at Lagardère Travel Retail, as well as to a decrease in trade receivables at Lagardère Publishing, especially in France and the United States, reflecting strong cash inflows in early 2018 (as a result of strong business momentum in the fourth quarter of 2017).

– Income taxes paid during the period totalled €11 million compared to €50 million in first-half 2017. The decrease in this item is primarily attributable to lower prepayments made in connection with tax consolidation in France, and to the impact of the dividend tax basis in the first half of 2017.

- Net disposals of property, plant and equipment and intangible assets

– Purchases of property, plant and equipment and intangible assets in first-half 2018 totalled €119 million (versus €125 million in first-half 2017), mainly relating to Lagardère Travel Retail (in line with its growth strategy), Lagardère Sports and Entertainment (acquisitions of sports rights) and Lagardère Publishing (namely the logistics streamlining project in the United Kingdom).

– Disposals of property, plant and equipment and intangible assets amounted to €202 million in first-half 2018, and essentially concern the sale of an office building in the eighth arrondissement of Paris (France).

- Free cash flow

– Free cash flow represented an inflow of €149 million in first-half 2018 (versus an outflow of €67 million in the prior-year period), with the difference mainly attributable to the improvement in working capital during the period, which includes the impact of the disposal of a real estate asset (net of taxes and relocation capex) representing a positive €193 million, versus a positive €143 million one year earlier.

- Net cash from financing activities

– Purchases of investments totalled €18 million in the six months to 30 June 2018, including notably the acquisition by Lagardère Active of a majority stake in Skyhigh TV, the leading independent production company in the Netherlands, and by Lagardère Travel Retail of railway station Foodservice stores in Austria. The remaining balance of this item corresponds to smaller-scale acquisitions and to a lesser extent, the payment of guarantee deposits and miscellaneous earn-outs.

– Disposals of investments, including interest received, totalled €23 million in first-half 2018, of which €17 million at Lagardère Active attributable mainly to the disposal of the 42% stake in the Marie Claire group.

FINANCIAL POSITION

At 30 June 2018, net debt stood at €1,453 million, an increase of €85 million compared to 31 December 2017 chiefly reflecting the traditionally adverse impact of seasonal fluctuations on working capital, offset by the disposal of a real-estate asset in the eighth arrondissement of Paris (France).

The Group’s liquidity position remains solid, with €1,879 million in available liquidity (available cash and short-term investments reported on the balance sheet totalling €629 million and an authorised but undrawn credit facility for €1,250 million).

IV- GUIDANCE

In view of the good performances observed in the first half of the year across all of the divisions and the outlook for the second half, the Lagardère group is raising the 2018 recurring EBIT target announced last March.

Group recurring EBIT growth in 2018 is now expected to be between 1% and 3% versus 2017(4), at constant exchange rates and excluding the impact of disposals at Lagardère Active.

V- KEY EVENTS SINCE 17 MAY 2018

As stated by Arnaud Lagardère and within the scope of the strategic refocusing plan:

- Closing of the sale of the Radio businesses in the Czech Republic, Poland, Slovakia and Romania

On 26 July 2018, the Group completed the sale of its Radio assets in the Czech Republic, Poland, Slovakia and Romania to the Czech Media Invest group. The sale price amounted to €73 million for consolidated revenue of around €56 million in 2017. - Conclusion of an agreement for the sale of magazine titles in France

On 26 July 2018, the Group entered into an agreement with Czech Media Invest with a view to selling certain magazine titles in France, namely Elle and its various extensions, including the online presence of Elle in France, Version Femina, Art & Décoration, Télé 7 Jours and its various extensions, France Dimanche, Ici Paris and Public. This agreement is subject to the prior reorganisation of the division, consultations with the relevant employee representative bodies, and clearance from the regulatory and competition authorities. - Disposal of the e-Health business

On 12 July 2018 the Group announced that it was preparing to sell its e-Health business at an enterprise value of €60 million (based on a 100% equity interest). MonDocteur has been sold to Doctolib and Doctissimo is subject to exclusive negotiations with the TF1 group aimed at concluding an agreement by 30 September 2018, subject to review by the relevant employee-representative bodies. - Disposal of the stake in Marie Claire

The Lagardère group disposed of its 42% in stake Marie Claire to Holding Evelyne Prouvost, the Marie Claire group holding company, via a share repurchase. - Acquisition of La Plage publishing house

On 16 July 2018, Hachette Livre acquired the entire share capital of La Plage, an illustrated books publisher in numerous domains (vegetarian, vegan, organic and gluten-free cookery books, organic cosmetics, natural therapies, etc.), on topics related to ethics and sustainable development.

VI- INVESTOR CALENDAR

- Third quarter 2018 revenue

Third-quarter revenue will be released on 8 November 2018 at 8:00 a.m. A conference call will be held at 10:00 a.m. on the same day.

(1)Alternative performance indicator, see definition at the end of the press release.

(2)Versus 2017 Group Recurring EBIT, restated for IFRS 15, at constant exchange rates and excluding the impact of disposals at Lagardère Active.

(3)Restated for IFRS 15, see appendices at the end of the press release.

(4)Restated for IFRS 15. See appendices at the end of the press release.

VII- APPENDICES

SECOND-QUARTER 2018 REVENUE:

CHANGES IN SCOPE OF CONSOLIDATION AND EXCHANGE RATES

First-half 2018

The difference between consolidated and like-for-like data is attributable to a €110 million negative foreign exchange effect resulting mainly from the depreciation of the US dollar, and to a €25 million positive scope effect, breaking down as:

- a €40 million positive impact from acquisitions, carried out mainly by Lagardère Publishing (acquisition of Bookouture representing a positive €5 million, Jessica Kingsley representing a positive €4 million, Summersdale representing a positive €3 million and IsCool Entertainment representing a positive €3 million), by Lagardère Active (acquisition of Aito Media Group representing a positive €4 million and Skyhigh TV representing a positive €3 million), by Lagardère Sports and Entertainment (acquisition of Brave Marketing Ltd representing a positive €3 million) and by Lagardère Travel Retail (consolidation of IFS stores in Poland and Citi Tabak in the Czech Republic, each representing a positive €4 million);

- a €15 million negative impact from disposals, mainly relating to the Press Distribution operations in Hungary (negative €11 million).

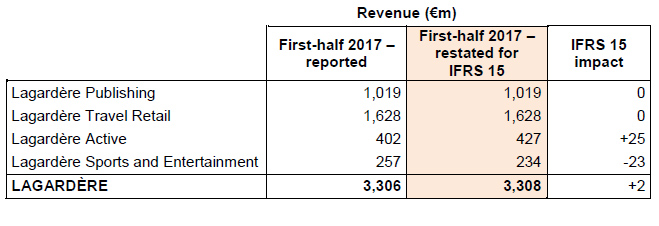

IFRS 15 RESTATEMENTS

The application of IFRS 15 had a €25 million positive impact on the reported first-half 2017 revenue of Lagardère Active and a €23 million negative impact on that of Lagardère Sports and Entertainment. The overall impact on consolidated first-half 2017 revenue was a positive €2 million.

The difference between first-half 2017 revenue restated for IFRS 15 and first-half 2017 revenue as published on 27 July 2017 can be explained as follows:

- restatements at Lagardère Active amounting to a positive €25 million, attributable to:

- commissions paid to third parties for distributing magazines and collecting subscriptions, which were previously deducted from revenue, are now recognised as an expense, with a positive impact of €16 million;

- the portion of revenue received by co-producers in the audiovisual production and circulation businesses, which was previously recorded as a deduction from external charges, is now recognised in revenue, with a positive impact of €9 million.

- restatements at Lagardère Sports and Entertainment amounting to a negative €23 million, attributable mainly to:

- signing fees for certain contracts, previously capitalised as sports rights assets and amortised, are now recognised in the balance sheet under advances paid and amortised as a deduction from revenue over the life of the contract, with a negative impact of €11 million;

- income received from sales of entertainment venue tickets, which was previously recognised for its total amount, is now only recognised for the commission invoiced by the Group in its capacity as agent, with a negative impact of €9 million.

- revenue generated under contracts for the sale of marketing rights with no other associated services, previously deferred over the life of the contract, is now recognised in full when the rights are actually sold, with a negative €3 million impact.

The change in the timing of revenue recognition at Lagardère Sports and Entertainment resulted in a €4 million decrease in recurring EBIT for first-half 2017, including €3 million in respect of revenue generated under contracts for the sale of marketing rights with no other associated services, which are no longer deferred over the life of the contract.

VIII- GLOSSARY

Lagardère uses alternative performance indicators which serve as key measures of the Group’s operating and financial performance. These indicators are tracked by the Executive Committee in order to assess performance and manage the business, as well as by investors in order to monitor the Group’s operating performance, along with the financial metrics defined by the IASB. These indicators are calculated based on elements taken from the consolidated financial statements prepared under IFRS.

- Like-for-like revenue

Like-for-like revenue is used by the Group to analyse revenue trends excluding the impact of changes in the scope of consolidation and in exchange rates.

The like-for-like change in revenue is calculated by comparing:

– revenue for the period adjusted for companies consolidated for the first time during the period and revenue for the prior-year period adjusted for consolidated companies divested during the period;

– revenue for the prior-year period and revenue for the current period adjusted based on the exchange rates applicable in the prior-year period.

The scope of consolidation comprises all fully-consolidated entities. Additions to the scope of consolidation correspond to business combinations (acquired investments and businesses), and deconsolidations correspond to entities over which the Group has relinquished control (full or partial disposals of investments and businesses, such that the entities concerned are no longer included in the Group’s financial statements using the full consolidation method).

The difference between consolidated and like-for-like figures is explained in section VII – Appendices of this press release.

- Recurring EBIT

The Group’s main performance indicator is recurring operating profit of fully consolidated companies (Group recurring EBIT), which is calculated as follows:

Profit before finance costs and tax

Excluding:

- Gains (losses) on disposals of assets

- Impairment losses on goodwill, property, plant and equipment, intangible assets and investments in equity-accounted companies

- Net restructuring costs

- Items related to business combinations

– Acquisition-related expenses

– Gains and losses resulting from purchase price adjustments and fair value adjustments due to changes in control

– Amortisation of acquisition-related intangible assets - Specific major disputes unrelated to the Group’s operating performance

= Recurring operating profit

Less:

- Income (loss) from equity-accounted companies before impairment losses

= Recurring operating profit of fully consolidated companies (Group recurring EBIT)

The reconciliation between recurring operating profit of fully consolidated companies and profit before finance costs and tax is set out in note 3 to the consolidated financial statements for the six months ended 30 June 2018.

- Operating margin

Operating margin is calculated by dividing recurring operating profit of fully consolidated companies (Group recurring EBIT) by revenue.

- Recurring EBITDA over a rolling 12-month period

Recurring EBITDA is calculated as recurring operating profit of fully consolidated companies (Group recurring EBIT) plus dividends received from equity-accounted companies, less amortisation and depreciation charged against intangible assets and property, plant and equipment.

The reconciliation between recurring EBITDA and recurring operating profit of fully consolidated companies (Group recurring EBIT) is set out in the presentation of the 2018 interim results.

- Adjusted profit – Group share

Adjusted profit – Group share is calculated on the basis of profit – Group share, excluding non-recurring/non-operating items, net of tax and minority interests, as follows:

Profit – Group share

Excluding:

- Gains (losses) on disposals of assets

- Impairment losses on goodwill, property, plant and equipment, intangible assets and investments in equity-accounted companies

- Net restructuring costs

- Items related to business combinations

– Acquisition-related expenses

– Gains and losses resulting from purchase price adjustments and fair value adjustments due to changes in control

– Amortisation of acquisition-related intangible assets - Specific major disputes unrelated to the Group’s operating performance

- Tax effects of the above items, including the tax on dividends paid in France

- Non-recurring changes in deferred taxes

= Adjusted profit – Group share

The reconciliation between profit – Group share and adjusted profit – Group share is set out in section II – Main income statement items.

- Free cash flow

Free cash flow is calculated as cash flow from operations plus net cash flow relating to acquisitions and disposals of intangible assets and property, plant and equipment.

The reconciliation between cash flow from operations and free cash flow is set out in note 3 to the consolidated financial statements for the six months ended 30 June 2018.

- Net debt

Net debt is calculated as the sum of the following items:

- Short-term investments and cash and cash equivalents

- Financial instruments designated as hedges of debt

- Non-current debt

- Current debt

= Net debt

The reconciliation between balance sheet items and net debt is set out in note 15 to the consolidated financial statements for the six months ended 30 June 2018.

A live webcast of the presentation of 2018 interim results will be available today at 18:00 p.m. (CET) on the Group’s website (www.lagardere.com).

The presentation slides will be made available at the start of the webcast.

A replay of the webcast will be available online later in the evening.

Press Contacts

Thierry Funck-Brentano - Tel: +33 1 40 69 16 34 - tfb@lagardere.fr

Ramzi Khiroun - Tel: +33 1 40 69 16 33 - rk@lagardere.fr

Florence Lonis - Tel. +33 1 40 69 18 02 - flonis@lagardere.fr

The Lagardère group is a global leader in content publishing, production, broadcasting and distribution, whose powerful brands leverage its virtual and physical networks to attract and enjoy qualified audiences.

It is structured around four business lines: Books and e-Books; Travel Retail; Press, Audiovisual, Digital and Advertising Sales Brokerage; Sports and Entertainment.

Lagardère shares are listed on Euronext Paris.

www.lagardere.com

Important Notice:

Some of the statements contained in this document are not historical facts but rather are statements of future expectations and other forward-looking statements that are based on management's beliefs. These statements reflect such views and assumptions prevailing as of the date of the statements and involve known and unknown risks and uncertainties that could cause future results, performance or future events to differ materially from those expressed or implied in such statements.

Please refer to the most recent Reference Document (Document de référence) filed by Lagardère SCA with the French Autorité des marchés financiers for additional information in relation to such factors, risks and uncertainties.

Lagardère SCA has no intention and is under no obligation to update or review the forward-looking statements referred to above. Consequently Lagardère SCA accepts no liability for any consequences arising from the use of any of the above statements.

Email alert

To receive institutional press releases from the Lagardère group, please complete the following fields:

Register